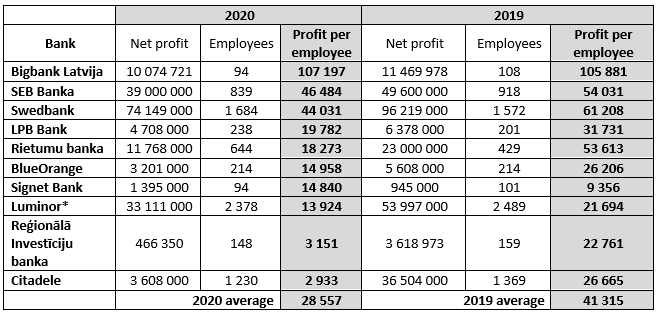

Adaptation to the unusual circumstances in the business environment has significantly affected banking sector operations: 8 out of 10 of Latvia’s largest banks experienced an drop in efficiency in the past year. In 2019, ten banks with the highest profit per employee earned EUR 41 315 on average, whereas in 2020, it was only EUR 28 557, which is 31% less than the year before. Only two banks – Bigbank Latvia and Signet Bank – managed to grow their efficiency in 2020.

Both of Latvia’s largest banks according to turnover – Swedbank and SEB Banka – are in the top 10 of banks with the highest profit, in third and second place respectively. At Swedbank, a 74 million euro profit has been accomplished by 1684 employees, or 44 031 euros each on average, whereas at SEB Banka, 39 million has been brought by 839 employees. This means that the average profit per employee was 46 484 euros. Bigbank Latvia is at the top of the rating, and its profit per employee is twice as high as that of the closest followers. Its 10 074 721 euro profit was provided by only 94 employees or 107 197 euros per employee on average. The year before, this result was 105 881 euros.

At Signet Bank, the joint effort of 94 employees brought a 1 395 000 euro profit or 14 840 per employee, which is a significant increase compared to 9 356 euros per employee the year before. In comparison, in 2019[EC1] , at Swedbank, the second most efficient bank, profit per employee decreased by more than 17 thousand, as in 2019 it was 61 208 euros, whereas in 2020, it was 44 031 euros. The drop at SEB Banka was more sparing – less than 8 thousand per employee, from 54 031 euros in 2019 to 46 484 euros in 2020, which allowed SEB Banka to climb to second place last year in the top of banks with the highest profit per employee. Whereas Citadele experienced the most dramatic drop in efficiency – from 26 665 euros in 2019 to 2 933 euros in 2020.

Net profit per employee in 2019-2020 (EUR)

Head of Bigbank Latvia Ģirts Kurmis explains the bank’s success with specialisation, focus and purposeful improvement of the company’s efficiency from the perspective of technical solutions as well as processes. High professionalism of the employees and their readiness to accept innovations is crucial in the achievement of these results, which allows the employees as well as the company to grow as a digital bank. Many long-term Bigbank Latvia employees, who have not lost their enthusiasm to find new solutions and reach even higher efficiency and profit, have played an important role.

“Since 2018, we have been determined and have improved the efficiency of our operations. The results are obvious. The technologies and efficient work processes introduced helped us quickly switch to distance mode at the beginning of the pandemic and continue productive work. This growth clearly shows the progress of our company at the strategic level as well as in the work attitude of our employees. While improving our performance efficiency, we are also trying to reduce insignificant costs and introduce technological solutions where possible,” explains Ģ. Kurmis.

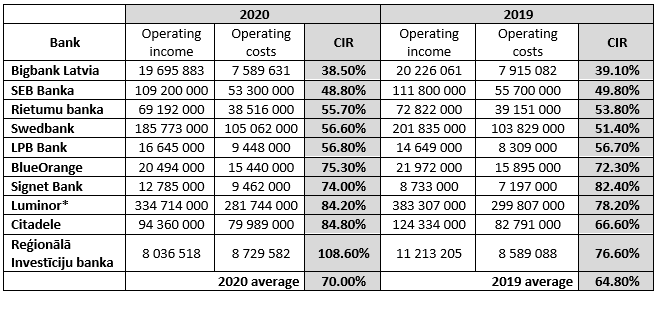

Efficient performance of Bigbank Latvia is also confirmed by another result. In 2020, it had the lowest cost to income ratio: 38.5%. Just like profit per employee, Bigbank Latvia managed to improve its performance in this parameter as well, as the year before the cost to income ratio reached 39.1%.

The closest followers in the CIR parameter are SEB Banka with 48.8%, improving performance by 1%, Rietumu banka with 55.7%, and Swedbank with 56.6%. The cost ratio of the latter two has grown in the past year, and this was the case for 7 out of 10 of Latvia’s banks with the highest profit. Reģionālā Investīciju banka has had higher operating costs than operating income in 2020. Overall, the average CIR of the 10 banks with the highest profit has significantly worsened during the year - from 64.8% to 70.0%.

CIR in 2019-2020 (EUR)

“Since Bigbank mainly specialises in issuing consumer credit without a guarantee, where the interest rate is higher than for mortgages with a good guarantee, and at the same time it has the low credit resources price available, which is characteristic for banks, Bigbank has a good markup margin, which is the basis for excellent profitability. The bank’s well-thought-out business model allows it to earn more than traditional banks or non-bank credit providers,” says economist and entrepreneur Jānis Ošlejs, “by applying modern management methods, such as 4DX and LEAN, as well as considering the fact that the bank operates without physical branches, and only as a distance service provider, with a highly-automated customer service and decision-making process, Bigbank manages to ensure very high performance and hence low costs. Traditional banks in Latvia continue to decrease their lending amounts, which is why Bigbank has the space and opportunity to increase its market share. Considering the business model chosen by Bigbank and its very successful implementation, the profit results are excellent.”

CIR is becoming a more and more significant criterion in the evaluation of the operations of banks and companies. It shows how well the company management is able to balance operating income and costs. In other words, how much money it has to spend to ensure turnover results. With humanity striving to reduce consumption to ensure the sustainability of our planet, companies are also expected to work more efficiently and achieve more using fewer resources.

Economics expert, former vice-chairman of the board at AS Hansabanka Uģis Zemturis states that a good CIR is around 40% and profit per employee depends on the bank’s activity profile. For example, Bank Norwegian, a Scandinavian consumer bank, has reached a CIR of 23%, and its net profit per employee is 2 million euros.

“If we analyse the CIR results of Latvia’s banks, these are not staggering – rather average compared to other markets. I would say, with such an average result, the banking sector is not very efficient. I suppose that the result has been negatively affected by Covid-19. Revenue has decreased or has not grown, but costs, mostly fixed, remained at the previous level. Banks that ensure a CIR of around 50% can feel fine. Their shareholders may be in the comfort zone. The not so impressive average CIR is negatively affected by 3 banks – Reģionālā Investīciju banka, Citadele, and Luminor,” analyses U. Zemturis, stating that “the biggest cost component for banks is employees and related costs. Theoretically, these are variable costs, but essentially they are permanent. This is why those banks whose business model is based on technologies can manage their costs easier in the case of business volume changes. There is a reason why digitalisation is at the top of the agenda.”

He emphasises that banks worldwide are focusing on issues of efficiency, and their management has to constantly deal with two questions - how to increase income and reduce costs. Banks also have credit risk management on their agenda. If the banking sector is at the stagnation stage - there is no significant development, growth of revenue is insignificant, the market has reached certain maturity and the number of clients is not growing, product usage activity is not growing - then the main focus is on performance. Here, however, we need to consider the fact that efficient performance is easier to achieve for specialised banks due to the nature of their activity.

“Corporate banks usually have a much smaller number of employees compared to the number of clients, and income from one client is much higher than for universal banks, and thus profit per employee is also significantly higher. However, costs per employee are higher than in universal banks,” says the former banker, emphasising that it is not really a good idea to compare specialised banks to universal banks.

Please enter your username and password.

2026 © The Baltic Times /Cookies Policy Privacy Policy