Following our foregoing articles about the Baltic Banking sector, in this issue we focus on the Lithuanian Banking sector. We analyse the balance sheets of the Lithuanian Banks and the data indicates the existence of seven regular Banks.

The largest players are, not surprisingly, the Scandinavian Banks, such as SEB Bank, Swedbank and DNB Bank. According to European data, Banks that have assets of more than 1 bn euros qualify as medium-sized. Apart from the Scandinavian Banks, another Lithuanian bank, namely AB Siauliu Bank, has assets more than 1 bn euros. The rest are small banks with assets less than 1 billion euros. In 2013, Lithuanian banking sector amounted to a little bit more than 18 billion euros. We have to emphasize that we do not take into account Banks that classify as ‘service providers from European Economic Area’. Regulators have separate “licences” for those structures establishing branch offices in a host country of the EU. They are exercising the Freedom of Establishment within the EU, and are thus subject to softer regulatory requirements.

The dominance of medium banks over the small banks in Lithuania is overwhelming. Medium banks have 96% of market share as measured by the size of the assets, and they provide 97% of the lending. As compared with 2008, in 2013 small banks in Lithuania have lost their market share both as measured by the size of the assets and in terms of lending activity. The extent of market concentration determines the business models particularly for small Banks. They lag behind medium Banks in terms of customer loan giving, but are more active than medium Banks in holding financial assets for trading. It could broadly signal that medium Banks focus on commercial banking, and small Banks have to differentiate towards more trading activities. The funding structures of Lithuanian banks are in line with the European banking sector’s benchmark. Both small and medium Banks have comparably high deposit ratios (68% and 64% of total balance sheet size) and equity funding (11% and 12% as measured in percentage of total assets). As seen from the profitability ratios (Return on Assets, Return on Equity), medium Banks in Lithuania were hit harder by the crisis in 2009. However, more stable funding structures and risk-adjusted growth of the balance sheet helped medium Banks to recover from the financial crisis relatively faster than small Banks.

Bank Business Models: The Asset-side structure

Typically, Bank Business Models differ in how assets are allocated between consumer lending activities, the so-called traditional banking activities and trading activities, the so-called investment banking activities. The Lithuanian banks’ customer lending activity is relatively high and ranges from 45% to 75% of total assets for individual banks. Contrary to the European Banking sector, the largest medium Banks are extremely focused on customer lending.

Yet, the largest medium Banks exhibit a lower proportion of net interest income to total income. In principle, one would expect that high consumer lending ratios would lead to high net interest income ratios as well. As an exception to these ratios, AB Bank “FINASTA” exhibits a customer loans ratio of only 13% of total assets. The Balance sheet data thus indicates that FINASTA is a typical investment bank. Indeed, the trading book amounts to 45% of total assets. Thus, in Lithuania all banks except FINASTA seem to follow traditional banking business given 1) their high proportions of customer loans and 2) comparably low positions in trading assets on the balance sheets (less than 20% of total assets).

In addition, the notional amount of derivatives for all Lithuanian banks, except FINASTA, is below a half a percent compared to up to 3000% of total assets for large European banks.European data shows that banks tend to invest in their trading books instead of taking the credit risks. According to the consolidated data on the evolution of assets for small and medium Lithuanian Banks, a minor reduction in basic lending activity in 2013 has been observed, exclusively for small Banks. In Europe, investment banks tend to have lower risk-weighted assets (RWA) than traditional commercial banks. In this respect, the Lithuanian data also differs from European data as FINASTA’s RWA are on the same footing than other Lithuanian banks.

Bank Business Models: The Funding-side structure

Apart from the way assets are allocated, the Banks Business models can also distinguished in the way Banks are funded. Overall, Lithuanian banks’ funding models are quite homogeneous. The bank’s funding base mainly consists of equity, deposits, and interbank exposures. Lithuanian bank leverage is broadly in line with the European benchmark. The equity ratios differ from 5% to 17% of total assets. The varying levels of leverage are not unusual since it costs more to hold the equity as a safeguard against financial disruptions than other sources of finance.

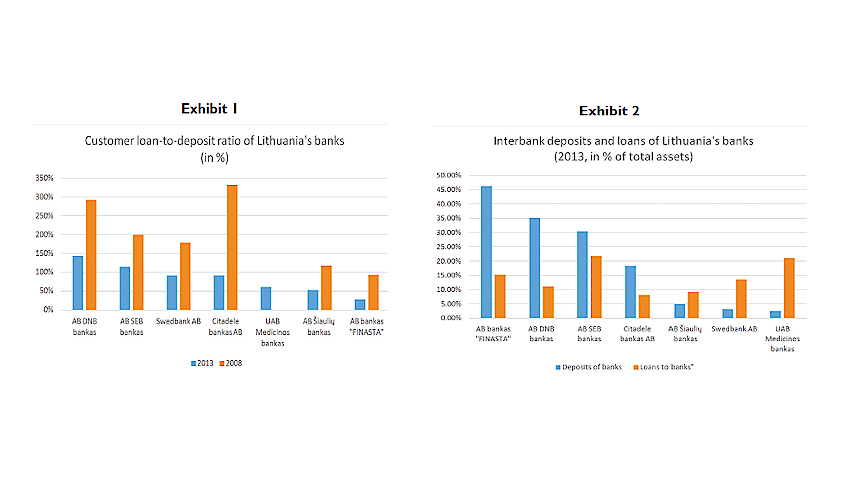

Typically, if leverage ends up below 4%, it starts to indicate eventual financial distress risks. The Lithuanian banks’ customer deposits ratios also seem “healthy” and do not warrant attention. They are even above the European benchmark, ranging from 46% to 85% of assets. Exhibit 1 indicates the banks’ customer loan-to-deposit ratio. A good benchmark is supposed to be around 80-90%. It means that the Bank is neither too aggressive, nor too conservative in terms of credit provision. The first thing apparent from the graph, is that between 2008 and 2013, there is a serious reduction in the credit provision activity to more sustainable levels.

In 2013, Swedbank and Citadele Bank were broadly in line with the typical benchmark. Otherwise, the data is still quite dispersed, ranging from 28% to 143%. It means that some of the largest medium banks, which had highest customer lending activity, are on the other edge in deposit taking from customers. Consequently, they lend more than a euro for every euro they bring in as deposits. At the other extreme, the investment bank FINASTA provides loans for less than one third for what is acquired through deposits. Their ratios still do not deviate too far from the Euopean ranges.

Customer deposits, however, are not the only source of funding used by the commercial banks. Lending and borrowing from interbank markets is also an important source of funding for Banks. In that respect, Exhibit 2 indicates that DNB Bank and SEB Bank interbank exposures through funding are relatively high, namely 30% to 35% of total assets. Smaller Banks, which have highest customer deposits, however, rank higher in terms of interbank loans. Bank FINASTA’s funding patterns, however, do not follow those models for the traditional commercial banks.

We observe that this bank does not seek to balance out the shortage in customer lending via interbank markets, rather it is the leader in interbank deposits. Overall, the interbank exposures in Lithuania reflect the European data in two aspects 1) the interbank deposits measured in % of total assets are higher than interbank loans, and 2) deposits are in broadly the same range. Deposit interbank funding implies greater stability for the banking sector than interbank loan activity. Finally, the consolidated data on medium banks’ evolution of liabilities shows an increase in customer deposits from 2008-2013 and indicates a relative stability of the Lithuanian Banking sector.

Business Models: Cross-border activities

So far we have split the Lithuanian banks according to their funding structures into traditional and investment banks. Another way to distinguish among banks operating in one territory is to look at their ownership and legal structures. However, they have little in common.

The difference starts when looking at the upper organizational structures of Lithuanian banks. Here we see that most of the medium Banks belong to larger banking groups headquartered outside the territory of Lithuania. Large Scandinavian groups such as Swedbank, SEB and DNB Bank own one hundred percent of their Lithuanian subsidiaries. Citadele Bank, the fifth bank in terms of assets, is fully-owned by Latvian-incorporated Citadele Bank. Only three out of seven Lithuanian banks are headquartered locally, AB Siauliu Bank, UAB Medicinos Bank and AB Bank FINASTA.

From the management perspective, these banks are quite different from each other. Most cross-border business models are somewhere in-between the centralized and decentralized approach to funding and liquidity management. The decentralized model implies that Banks’ subsidiaries refinance themselves and are largely autonomous in terms of capital and liquidity management. The centralized model, on the other hand, implies a high degree of centralized wholesale funding through the parent bank in its home state and a coordinated liquidity management. In reality, however, more often a coordinated model, which includes elements from both approaches, is used. In the case of the Baltic States, the centralized approach plays an overwhelming role, notably due to the market proximity with Scandinavian countries and the degree of regional integration.

Apart from the large Banks’ subsidiaries, locally incorporated banks occupy a minor market share in Lithuania. Moreover, AB Siauliu bankas, UAB Medicinos bankas do not pursue cross-border activities. That seems a little bit strange provided that AB Siauliu bankas is the fourth largest bank after the three Scandinavian subsidiaries in Lithuania with assets more than one billion euro. When we analyze the ownership structure of AB Siauliu bankas, it seems quite dispersed – top10 major shareholders own almost 53% of the shares. The largest institutional ownership amounts to almost 20% of shares. There is a relatively high extent of institutional ownership among largest shareholders (70%).

In contrast, UAB Medicinos bankas has two major shareholders, the largest of them holding nearly 90% of shares. Institutional ownership constitutes almost 10%.

Overall, a major part of Lithuanian banking sector is fully owned outside its territory, but does not reach outside the European Economic Area. This fact, however, determines the decision-making processes of those banks. Local Lithuanian banks are inactive in their cross-border activity. In fact, smaller Banks are very different in their characteristics with regard to ownership structures.

Dr. Michel Verlaine is managing director of SLF Specialists in Law and Finance (www.slf.eu.com) and associate Pr. of Finance at ICN Business School (www.icn-groupe.fr ).

Alina Rekena is a consultant at SLF Specialists in Law and Finance.

Please enter your username and password.

2026 © The Baltic Times /Cookies Policy Privacy Policy