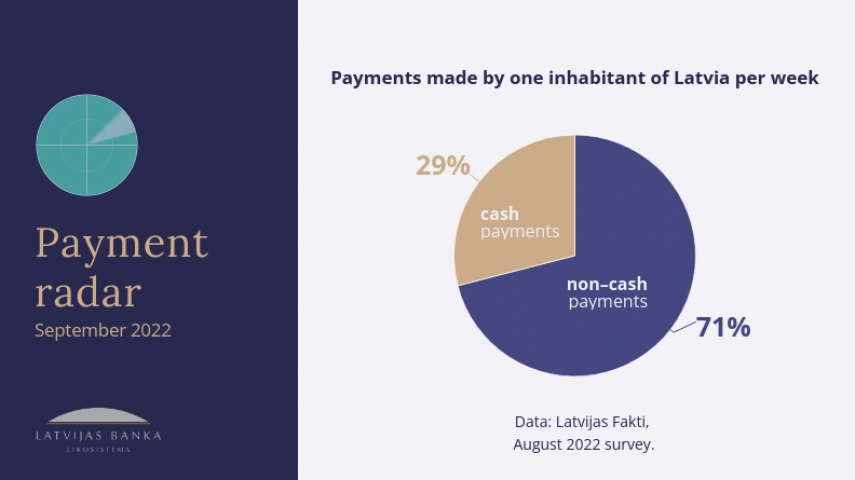

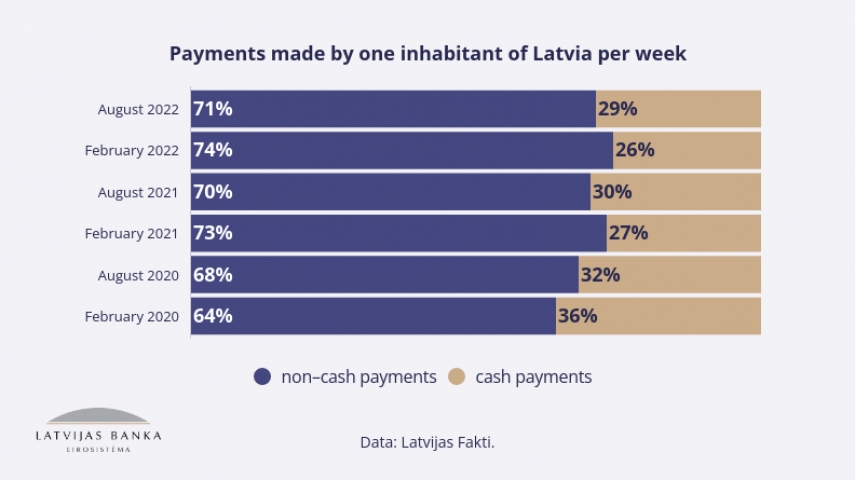

The most recent (August 2022) "Payment Radar" of Latvijas Banka suggests that the ratio of non-cash and cash payments in Latvia was 71% to 29% in late summer of 2022.

The "Payment Radar" contains the latest information on money usage habits of Latvia's households, businesses and the public at large. This information has been obtained from the results of the population survey conducted by a market and social research agency SIA Latvijas Fakti.

The "Payment Radar" is published semi-annually and available on Latvijas Banka's website (https://www.bank.lv/en/tasks/payment-systems/payment-radar). Changes in the proportion and interaction between non-cash and cash payments (as at August 2022) is the central measurement of the overview supplemented by more detailed numerical information and experts' commentaries.

August 2022 exhibited stability with regard to all major measurements of money use. Compared with February 2022, the use of cash has somewhat increased. The ratio of cash and non-cash payments was then 74% to 26% (70% to 30% in August 2021). In August 2022, the average number of payments made by one inhabitant per week stood at 12.6 (12.8 in February 2022, 13.9 in August 2021).

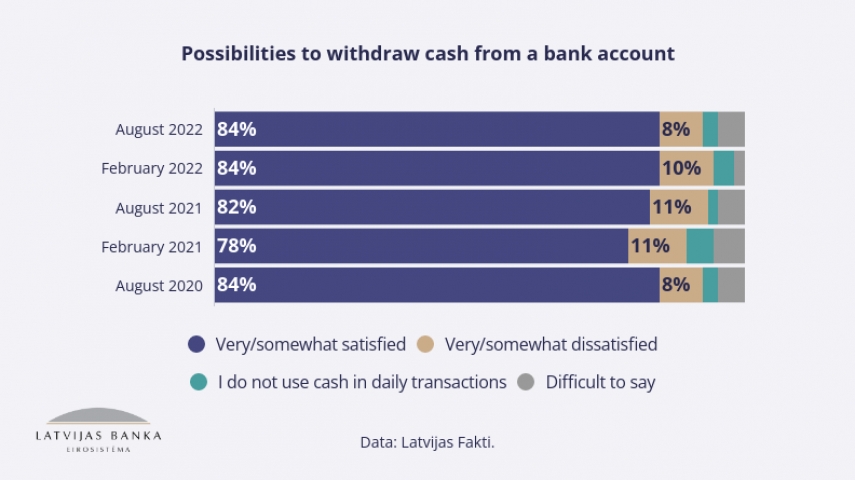

Public satisfaction as regards a possibility to withdraw cash from bank accounts remains stable. In August 2022, 84% of those surveyed by SIA Latvijas Fakti were completely or rather satisfied with cash availability. The figure is the same as in February 2022 and exceeds that of August 2021 by two percentage points. At the same time, the number of people dissatisfied with the possibilities to withdraw cash from their bank accounts continues on a downward path (8% in August 2022, 10% in February 2022, 11% in August 2021).

Zita Zariņa, Member of the Council of Latvijas Banka, points out in the expert commentary section that ensuring cash availability has been one of the priority areas of Latvijas Banka for the past two years. In September 2021, the general public learned about the agreement reached in the financial sector on ensuring cash availability to residents of Latvia. The aim of the Memorandum was to ensure cash availability to residents across the entire territory of Latvia, setting the minimum requirements for availability and reachability of cash.

A year has passed, and it is possible to take stock of the progress made towards the attainment of the aims of the Memorandum. There were 902 ATMs in Latvia during the drafting of the Memorandum. A year later, in autumn 2022, their number has seen an insignificant decrease (by 1%) – to 894. It can thus be concluded that the financial sector has honoured its commitment to refrain from reducing the number of ATMs by more than 5%.

"Why does Latvijas Banka pay particular attention to the issue of cash availability? Because it not only affects the public's freedom of choice but also strengthens Latvia's economic security which is especially relevant at present when Russia has launched war on Ukraine. Cash is part of the critical financial sector infrastructure; therefore, we continue our cooperation with the sector to implement measures ensuring access to cash in "times of peace" and be ready to ensure the population's access to its money in times of crisis", emphasises Zita Zariņa.

Discussions with partners from Finance Latvia Association and Latvia's leading commercial banks are ongoing to agree on the next steps towards ensuring cash availability, including continued implementation of the measures that were defined and successfully implemented in the context of the Memorandum of Understanding concluded in 2021.

The measurements of people's attitude towards small denomination euro coins are stable. In February 2022, 51% of those surveyed expressed the view that 1 and 2 cent coins should be withdrawn from circulation, 43% – that they should remain in circulation, but 6% of the respondents were unable to form their opinion. In August 2022, 49% of the population supported the withdrawal of small denomination euro coins from circulation, 43% were against it, while 8% of the population were unable to form their opinion. In the course of a year, the number of the population supporting the withdrawal of 1 and 2 euro cent coins from circulation has rather strongly increased. In August 2021, the withdrawal of small denomination coins from circulation was supported by 43% of the population, 50% of the respondents pointed out that these coins should be retained in circulation, but 7% of those surveyed found it difficult to express their views.

The "Payment Radar" contains several commentaries on topics relevant to society concerning cash circulation. The recent trends observed in development of the use of cashless money and cash have been commented by Aigars Freimanis, Director of SIA Latvijas Fakti; cash availability – by Zita Zariņa, Member of the Council of Latvijas Banka; topical issues concerning the introduction of the digital euro – by Emīls Dārziņš and Reinis Vecbaštiks, state-of-the-art payment experts of Latvijas Banka; Croatia's path towards joining the euro area on 1 January 2023 – by Miķelis Zondaks, economist of Latvijas Banka. The "Payment Radar" includes visual materials of Croatian euro coins that will also reach our wallets after the turn of the year.

COMMENTARY SECTION

Aigars Freimanis, Director of SIA Latvijas Fakti: A growing section of society prefers making daily payments using formats provided by modern technological development

The measurement of the Payment Radar in this August continues to show the previously-observed trends of decline in cash payments and a growing prevalence of more modern payment systems. The gradual decline in the share of cash payments is evident in absolutely all key socio-demographic population groups, i.e. groups in terms of age, education, income, both, in urban and rural areas.

It can also be observed that the number of users of contactless bank cards, smartphones and instant payments is growing. An increasing proportion of the society prefers formats provided by the development of modern technologies for daily payments. Younger people, as well as those having a higher level of education and income, are traditionally more open to new technologies. In these audiences more than 70% of respondents use contactless payment cards for payments, more than 40% of respondents make money transfers by instant payments, and one in five respondents makes payments on smartphone.

At the same time, in August, the number of payments made online during the survey week had decreased. This probably provides evidence in favour of the convenience provided by good mobile technologies and the fact that convenience of life, speed of processes and rational functionality have a greater impact on the changing behaviour and habits of consumers than such factors as safety, stability and a full control of the situation.

Zita Zariņa, Member of the Council of Latvijas Banka: Cash availability: achievements and plans

In September 2021, the general public learned about the agreement reached in the financial sector on ensuring cash availability for residents of Latvia. The Memorandum of Cooperation in this area was signed by Latvijas Banka, Finance Latvia Association and the commercial banks having the widest network of ATMs and branches: Swedbank AS, AS SEB banka, the Latvian branch of Luminor Bank AS and AS Citadele banka.

The aim of the Memorandum was to ensure cash availability for residents across the entire territory of Latvia, setting the minimum requirements for availability and reachability of cash. The signatories of the Memorandum agreed on the following course of action to ensure cash availability throughout Latvia:

- preserve the existing network of ATMs and refrain from reducing the number of ATMs by more than 5% until 1 January 2023;

- when creating the network of ATMs, the straight-line distance from any location to the closest ATM should overall not exceed 20 kilometres for 99% of Latvia's population;

- ensure adequate actual accessibility of ATMs to consumers (at least 12 hours a day).

A year has passed and it is now time to look back at the progress made in achieving the aims of the Memorandum.

There were 902 ATMs in Latvia during the drafting of the Memorandum. A year later, in autumn 2022, their number has seen an insignificant decrease (by 1%) – to 894. It can therefore be concluded that the financial sector has honoured its commitment to refrain from reducing the number of ATMs by more than 5%.

The population survey conducted in August 2022 by SIA Latvijas Fakti helps to assess the population's satisfaction with the possibilities of accessing cash. Within a year, the share of people satisfied with their possibilities of withdrawing cash from their accounts has risen from 82% to 84%. In comparison with the data from the survey conducted in February, changes in this figure have not been observed this year. At the same time, there is a continuous decline in the share of respondents dissatisfied with the possibilities of withdrawing cash from their accounts. In August 2021, 11% of respondents expressed their discontent compared with 10% in February 2022 and 8% in August.

Why does Latvijas Banka pay particular attention to the issue of cash availability? Because it not only affects the public's freedom of choice but also strengthens Latvia's economic security which is especially relevant at present when Russia has launched war on Ukraine. Cash is part of the critical financial sector infrastructure; therefore, we continue our cooperation with the sector to implement measures ensuring access to cash in "times of peace" and be ready to ensure the population's access to its money in times of crisis.

At present, while continuing our successful cooperation with partners from Finance Latvia Association and Latvia's leading commercial banks under the Memorandum of Understanding concluded in 2021, we are planning specific further steps towards ensuring cash availability also in the future.

Cash is and will remain a significant payment and savings instrument. The development of non-cash means of payment will not change this situation; the public will only benefit from extended and complemented freedom of choice and convenience.

Reinis Vecbaštiks, Emīls Dārziņš, State-of-the-art Payment Experts at Latvijas Banka: Digital euro – how much have we achieved?

It has been almost one year now since the Eurosystem launched the digital euro investigation phase. During the study, the European Central Bank (ECB) closely cooperated with the euro area member states and market players to decide on the technical and practical aspects of the digital euro. During this stage, decisions on the design or the technical solution and the functional framework of the digital euro are made, as well as on its added value for the current electronic payments. It is expected that the investigation phase will complete in October 2023, and then a decision will be made on launching the practical introduction of the digital euro.

The ecosystem already has a mixed payment model where the central banks ensure the monetary foundation (deposits to commercial banks and cash to people), while the private sector offers payment solutions to its customers (payment cards, digital apps, etc.). These solutions are based on the financial means of commercial banks (deposits).

An important element of this model is the opportunity at any time to convert private money (provided by commercial banks) into public money or the money of the central bank 1:1, as well as to use this public money to make payments. The guaranteed convertibility contributes to and maintains the trustworthiness of the private and public money. This model ensures that the currency functions as a single payment system. Thus, the money of the central bank serves as a monetary anchor that maintains a functioning payment system and ensures the financial stability and trust in the currency.

Currently, the money of central banks is available to the public in the form of cash. Therefore, during the digital age, when the share of the digital money is on the rise, cash becomes less relevant as a means of payment.

If there is no stable monetary foundation for digital payments, the growing demand results in challenges to the European strategic autonomy and monetary independence, including due to the fact that most electronic payment solutions are offered by companies headquartered in third countries. Global technological companies are able to rely on their huge customer base to introduce stable crypto coins that might theoretically destabilise the current financial system and increase the risk of the payment market being dominated by third-country solutions and technologies.

The digital money of central banks (central bank digital currency or CBDC) is a hot item not only in Europe, as a large number of central banks in the entire world work on such projects. Moreover, several countries have already reached the practical implementation stage or have already introduced the CBDC. Nigeria is one of such countries, as in October 2021 it became the first African nation to emit its CBDC: eNaira. As to countries of particular importance for the global economy, China was the first to start practical testing of the national digital currency as early as in 2020.

In Europe, Sweden takes the lead concerning the introduction of CBDC: it started the research phase for the digital krona already in 2017 and has already reached the stage of technical testing.

Digital euro not only aims to improve the efficiency of digital payments but also to maintain the local and international competitiveness of the euro, assuming that the payment digitisation trend, as well as the range of external supply will keep growing. However, it is too early to claim that practical introduction will start after the investigation phase of the digital euro. It will depend on the results of the research, as well as the final decision of the European Union (EU) policy makers.

Public interests are given priority in shaping the digital euro during the investigation phase. To achieve this goal, the ECB studies the public opinion and wishes concerning the introduction of the digital currency of central banks.

In April 2021, the results of the public consultation on the digital euro project were published. The report concluded that the respondents considered easy use of the digital euro in the entire euro area and privacy of payments its main functional features.

Privacy is one of the fundamental rights, thus, in developing the design of the digital euro, the Eurosystem strives to meet the highest possible standards. During the investigation phase, various tools to ensure comparable functionality of the digital euro and cash are assessed. However, privacy is also considered in the context of several other EU policy targets, in particular for the purposes of AML/TCF.

For the digital euro to succeed, during the investigation phase it is important to thoroughly review the potential impact of the digital euro on the monetary policy, financial stability and financial intermediation services. Any unwanted consequences for the monetary policy and financial stability should be precluded already in the design stage.

For example, one such area is deposits, thus, options to prevent their outflow after the introduction of the digital euro are considered. Quantitative restrictions on individual deposits are considered as one of potential instruments to avoid the use of the digital euro as a means of financial investment. In addition, dissuasive conditions for deposits in the digital euro are also considered if they exceed a specific threshold.

At the same time, by developing these tools the Eurosystem aims to ensure simplicity both in technically implementing the digital euro, as well as from the point of view of user experience. As the private sector is the most important source of innovation and efficient products and services for customers, the Eurosystem expects that monitored financial services providers will play a significant role is distributing the digital euro to end users.

At the same time, a compromise will have to be achieved in deciding about the legal framework of the digital euro since it has several objectives: e.g. the right to privacy and public interest in maintaining a certain degree of supervision to eliminate unlawful activity. The design of the Eurosystem digital euro also aims to efficiently balance the advantages of extensive use of the digital euro and the need to provide financial intermediation services and stability.

From the point of view of use, several options of the digital euro are considered during the investigation phase, e.g. mobile apps and online banking, as well as individual digital wallets. The digital euro should also benefit the part of the society that has limited access to the financial services to make and receive digital payments and contribute to financial inclusion. We still have to discuss and agree on a specific solution for the digital euro, and how it will reach every person and every business.

Finally, the introduction of the digital euro would give the euro area residents access not only to cash but also to the digital money of the central bank that guarantees its security and efficiency in daily use. Remember that cash is not in danger and that the Eurosystem has undertaken to continue its use. The digital euro does not aim to replace any other type of money (cash or non-cash), but to complement them and offer new opportunities.

The investigation phase of the digital euro will continue until October 2023, and then the final decision will be made on whether to begin the implementation of the digital euro project. Following the adoption of this decision, testing and development may also start.

We invite you to follow the progress of the investigation phase also on the ECB website.

The economic conference hosted by Latvijas Banka on 3 November 2022 will also discuss more widely the future of money, including digital currencies. All those interested are invited to follow the conference online on www.macroeconomics.lv.

Miķelis Zondaks, Economist, Latvijas Banka: Welcome to the euro family!

On 12 July 2022, the Council of the European Union (EU) adopted a historical decision on the admission of Croatia to the euro area on 1 January 2023. Croatia will become the 20th Member State of the euro area (Latvia joined the euro area as the 18th Member State and introduced the euro on 1 January 2014, followed by Lithuania a year later).

Taking account of Croatia's timely and long-lasting preparation, it is quite safe to say that the introduction of the euro will not turn the daily life of the country's population upside down which in fact is to be welcomed. The key benefits are the ones people do not even see in their everyday lives; these include much lower costs of transactions with other euro area Member States, a reduced currency risk and a strengthened economic resilience to crises. Over almost nine years, we have witnessed it all in Latvia where there are no concerns about the stability of currency despite several economic shocks experienced during this period, for instance, the pandemic and two attacks on Ukraine by Russia.

Hrvatska narodna banka has pursued for a long time a policy of maintaining a relatively stable exchange rate of the Croatian national currency – the kuna – against the euro. Moreover, even before the introduction of the European single currency, most household deposits (87%) and nearly all external debt (90%) are in euro which means that the reduced currency risk will be a great benefit. Businesses find themselves in a similar situation: they not only borrow in euro but quite often also indicate the prices of goods and services in euro (for instance, in the fields of real estate, vehicles, accommodation, etc.).

Seeing how widely the euro is currently being used in the Croatian economy, a question about the not-so-strong support by the population for the introduction of the euro may arise; however, these statistics should be examined in conjunction with Croatia's situation as a whole. According to the Eurobarometer survey conducted in summer 2022, 52% of Croatia's citizens support a single currency in the EU – a lower level than the average in the EU (72%). At the same time, this indicator can be viewed as relatively high among the countries that have not yet introduced the euro (for instance, 33% in the Czech Republic). Moreover, since the beginning of the year, the number of respondents against the single currency has decreased by 4 percentage points (to 40%). It should also be taken into account that Croats are rather sceptical about many things, including the EU as a whole: according to the Eurobarometer survey, only 42% of the respondents have expressed trust in the EU (which is still twice as high as the indicator of trust in their own government and parliament). Thus, it can be concluded that the accession of Croatia to the euro area will be quite smooth and the scepticism can most likely be explained by the overall low level of the population's trust in various national and international institutions.

This enlargement of the euro area will not result in significant changes in the daily lives of Latvia's population, mostly due to the geographical distance. The impact will become apparent in several areas. Firstly, we will directly witness the above mentioned reduced transaction costs during tourist trips, as in future all prices will only be indicated in euro and there will be no concern over currency exchange and exchange rate. A small, yet pleasant matter. Furthermore, as a continued integration in the EU, Croatia also plans to join the Schengen area which over time would make travelling even more comfortable. Secondly, every new euro area Member State adds to the significance and role of the euro in the international economy. This, in turn, strengthens the euro as a whole and thus increases the economic resilience of Latvia, Croatia and the whole euro area to crises.

Meanwhile, the people captivated by coin collection will find a new area of work: to obtain the new Croatian euro coins that are currently being minted by the local mint. The reverse of the 2 euro coin will feature the map of Croatia, while the reverse of the 1 euro coin will depict a marten. A marten was chosen to honour the existing national currency, the kuna (the word kuna means "marten" in Croatian), whose name is, in turn, connected with the fact that historically, during the Middle Ages, marten skins were used as a means of settlement. The euro cent coins will display the portrait of Nikola Tesla and letters HR in the Glagolitic script.

It is expected that Bulgaria, already preparing for the introduction of the euro, will be the next to follow Croatia's example. This will further strengthen the positions of the euro as the second most significant global currency (alongside the US dollar).

The sociological survey data and detailed information are available at https://www.bank.lv/maksajumu-radars.

Please enter your username and password.

2026 © The Baltic Times /Cookies Policy Privacy Policy