At the June monetary policy meeting, the management of the European Central Bank (ECB) decided not to change interest rates for the euro and to end the purchase of net assets under the Asset Purchase Programme (AIP) on 1 July 1, 2022 (i.e., no more money will flow into the market). In addition, ECB indicated its intention to raise key interest rates by 25 basis points at its July 21 monetary policy meeting and has already committed to raising rates at its 8 September meeting. However, the extent of the September hike will depend on the medium-term inflation outlook.

Along with the central banks of Japan and Switzerland, ECB is among the few central banks that have not yet touched on interest rates. A number of central banks have already raised interest rates in the past year (Figure 3.).

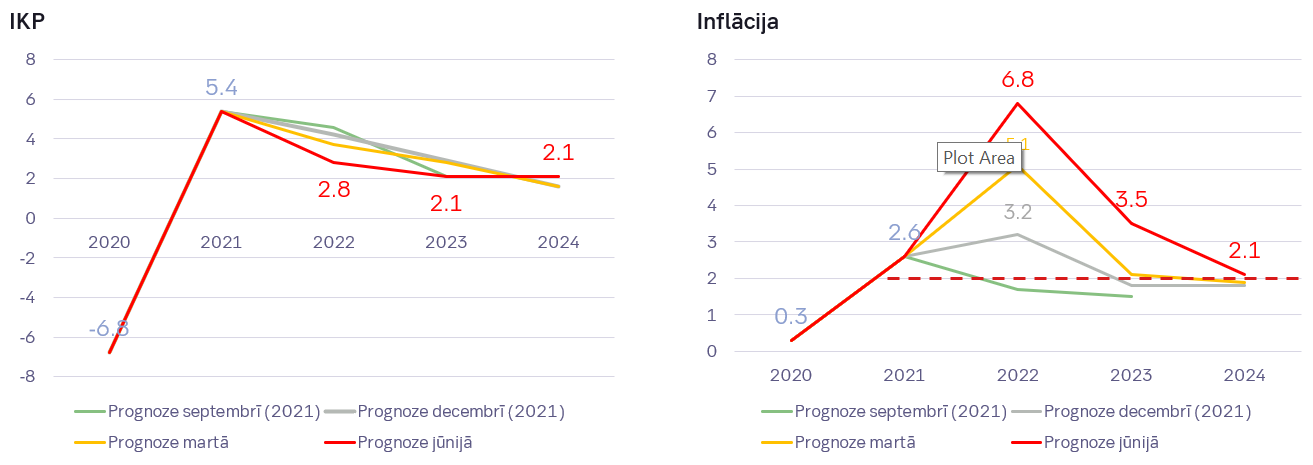

This month, the ECB also released the latest GDP and inflation forecasts for the Eurozone. As expected, the inflation forecast for this year was revised significantly upward to + 6.8%, while the GDP figures were revised downward to + 2.8% (Figure 2). The high inflation rate is mainly due to the sharp increase in energy and food prices, including the wartime intensification of inflationary pressures, which has led to a sharp increase in the prices of many goods and services, according to ECB. The ECB believes that the eventual decline in energy prices, reduction in pandemic supply disruptions, and normalisation of monetary policy will help to reduce inflation.

Conclusions on loans

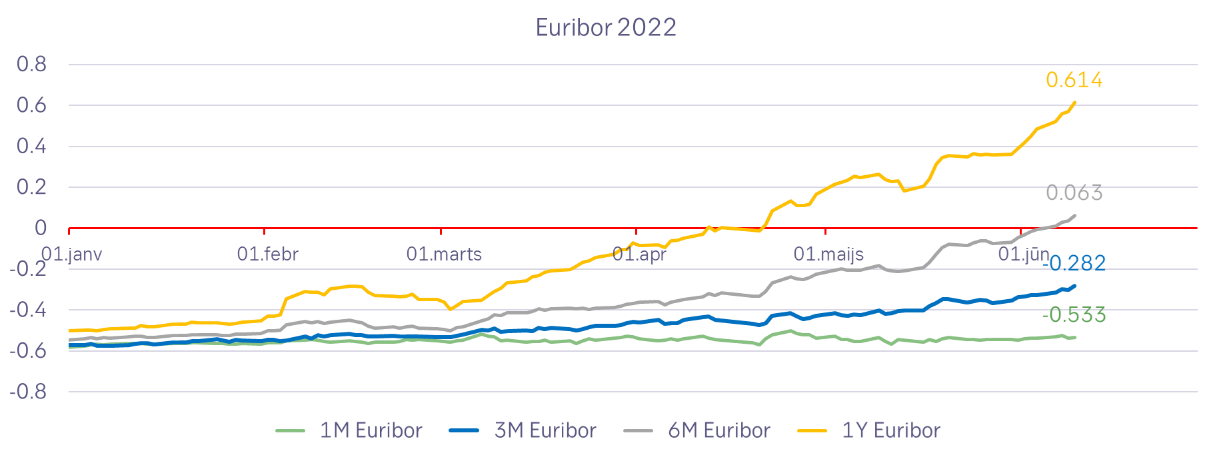

Again, the pain is evident, as a look at the euro interest rate tables shows positive rates in the market long before the ECB planned interest rate changes. (Figure 1). The 1-year Euribor rate already slipped into positive territory in April, and the 6-month Euribor rate remained positive in the first days of June. The promised increase of 25 basis points means that monthly interest payments on a loan of 50 thousand euros should increase by about EUR 10 (EUR 120 p.a.), but on the market, the 1-year Euribor has already exceeded 0.60%, which corresponds to the annual interest cost of EUR 50 thousand. Compared to the situation a few months ago, the increase is already about EUR 300.

In real life, all this is not so simple, because normally the loan principal is repaid gradually, reducing the interest payments at constant interest rates. At present, however, market prices suggest that the negative effects of rising interest rates will outweigh the positive effects of repaying the loan incrementally (i.e., higher interest will be charged on the smaller remaining loan principal ). Currently, it looks like the popular 3-month Euribor could be above 1.50% next year. Of course, much depends on how the war in Ukraine develops and what happens to consumption, wage growth, and economic growth. One of the negative side effects of high interest rates is the risk of an economic slowdown and recession.

Conclusions on deposits

Gradually, it may well be that something more than zero will come out in the field of euro deposits. But the change will not be fast, because against the background of the expected increase in euro interest rates, there are consequences of "printing" money that took place in recent years. The market is characterized by a surplus of euros, as evidenced by the fact that the shortest maturity of euro interest rates in the market is at or below the ECB deposit rate of -0.50%. If the "retail" market has to wait longer for positive interest rates, then positive "wholesale" rates can already be observed today, but then we are speaking of long maturities (about one year and longer). The notional "surplus" of the euro can also be observed in Latvia, as according to the Bank of Latvia, Latvian households and enterprises (non-financial companies) had borrowed EUR 10.38 billion at the end of March, while EUR 16.8 billion was available in their accounts. The ratio of deposits to loans is 62%, which is very low and reduces the demand for deposits in the financial markets

Expecting severe winter

The high level of deposits is good news because high energy prices, rising food prices and rising interest rates will triple consumers' wallets, making it easier to bear with a larger account balance. But the trio will likely have a negative impact on economic growth (which is why the ECB, the World Bank, the OECD and a number of other global institutions have recently lowered their GDP forecasts), while in some cases reducing the willingness to lend in such a risky market. Money for loans is available, only its price is rising, and the assessment of risk may become more cautious.

Figure 1. Dynamics of Euribor interest rates for various maturities in 2022.

Figure 2. Current and historical ECB’s GDP and inflation forecasts

Figure 3. Base rates of various central banks over the past year

Please enter your username and password.

2026 © The Baltic Times /Cookies Policy Privacy Policy